To pay Chinese golf ball manufacturers safely, treat payment as a buyer-control system, not just a payment method. Verify the supplier’s legal entity and beneficiary name, lock bank details in a signed PI or bank annex, attach specs and artwork before deposit, release the balance only after PSI pass and verifiable shipping documents, and stop every bank-change request until independently verified.

T/T, escrow, card, and L/C can all be useful, but none is automatically safe. The real risk is paying the wrong beneficiary, accepting editable bank instructions, approving a deposit before specs are locked, or sending the final balance before objective proof exists.

Use this guide to turn T/T, deposit, balance, PSI, bank-change checks, and repeat-order payments into an auditable buyer SOP for golf ball OEM sourcing.

Why does payment risk start before wiring?

You may think payment risk begins when your bank sends the wire, but the real danger starts earlier if nobody owns identity checks, bank details, specs, PSI, and shipping proof.

Payment risk starts before wiring because your team must verify who gets paid, what was approved, and what proof releases the next milestone. T/T is not the core danger; uncontrolled beneficiary names, editable bank instructions, weak PI terms, and no PSI gate are.

Paying a Chinese golf ball manufacturer safely means preventing two failures: paying the wrong recipient and releasing funds before objective proof exists. That is a finance control process, not a trust exercise.

Cross-border payment risk is not theoretical. In the 2024 Internet Crime Report, reported losses exceeded $16 billion, and losses increased sharply from the prior year. For a first golf ball OEM order, the practical lesson is simple: a familiar email thread, an urgent invoice, or a last-minute bank update should never outrank your payment-control rules.

Assign owners before money moves. Sourcing verifies the supplier’s legal identity. AP locks the beneficiary name and bank details. QC defines what “PSI pass” means. Logistics checks shipping documents. Management approves exceptions. If one owner is missing, the wire is not ready.

| Pain/decision | Owner | Control proof | Action/evidence |

|---|---|---|---|

| Supplier identity | Sourcing | Legal entity + business record | Save verification |

| Bank recipient | AP/finance | Beneficiary name match | Lock vendor file |

| Spec approval | Buyer/QC | Spec annex + sample approval | Attach to PI |

| Balance release | QC | PSI pass | Hold until pass |

| Shipping proof | Logistics | Draft B/L or forwarder proof | Verify before release |

| Bank change | AP + manager | Phone/video + signed amendment | Hard stop |

A buyer-control file should also define basic terms. T/T means telegraphic transfer or bank wire. PI means Proforma Invoice. Beneficiary name means the legal bank-account recipient. Escrow or Trade Assurance means a platform-controlled release path when eligible. L/C means bank payment against compliant documents. These are useful tools, but none replaces the control chain.

✔ True — Safe payment is a control system

The method matters, but the controls matter more. Your team needs verified identity, locked bank details, written release triggers, PSI evidence, and shipping-document proof.

✘ False — “T/T is automatically unsafe or automatically safe”

A wire to a verified company account with staged release gates can be controlled. A wire based on editable email instructions is not controlled.

Who owns AP, sourcing, QC, and logistics?

Your payment process is only as safe as the weakest owner in the chain.

Create a role-based payment-control sheet before the deposit. Each row should show the owner, required proof, payment status, and exception approver. Then check whether each team can produce its artifact before the wire is released.

Do not initiate payment until identity, bank details, PI, spec annex, and release milestone are assigned to an owner.

Which method fits your order risk?

You may ask which payment method is safest, but no method protects you if the beneficiary is wrong, the bank details are editable, or the balance is released before inspection.

The safest method is the one your team can control with evidence. For samples, card or small T/T may be practical; for bulk, verified-company T/T or escrow may work; for high-value orders, L/C can add document control, but none replaces PSI and bank-lock rules.

Payment methods are rails. They move money. They do not define product specs, approve logo samples, inspect cartons, verify beneficiary names, or stop bank-account changes by themselves. That is your team’s job.

For samples, a small payment method can keep admin simple. For tooling or mold fees, T/T to a verified company account may be normal because the supplier needs funds before production. For a first bulk order, escrow may add comfort when the order qualifies, while T/T can work if the beneficiary, PI, bank annex, PSI, and shipping triggers are locked. L/C can support larger documentary transactions, but paperwork and bank review can slow a custom golf ball order.

A higher deposit may help with MOQ, capacity, or priority, but it is a cash-flow risk exchange, not a free benefit. If you increase exposure, your team should receive a clearer production calendar, sample milestone, inspection rights, and balance-release proof.

| Pain/decision | Best-fit method | Risk control | Action/evidence |

|---|---|---|---|

| Small sample | Card/PayPal or small T/T | Limit exposure | Verify recipient |

| Tooling/mold fee | T/T to verified company | Written milestone | Approve drawing/sample |

| First bulk order | Escrow or T/T | PSI before balance | Gate release |

| High-value shipment | L/C | Document control | Use bank review |

| Higher deposit request | Negotiated T/T | Cash-flow trade-off | Ask capacity/PSI terms |

T/T, escrow, L/C, or card?

Your method choice should reduce risk without pretending the payment rail replaces control.

Request method-specific quote terms that state deposit, balance, proof required, fees, timing, and remedy path. Then check whether the method matches the order value and whether your team can execute the evidence gates.

Do not select a payment method until identity match, bank-lock, release milestone, and dispute path are visible.

What should the PI lock before deposit?

You may be asked to pay a deposit quickly, but the deposit becomes dangerous if the PI does not lock specs, artwork, lead-time start, bank details, and acceptance triggers.

A deposit should start a controlled production path, not a vague promise. Before your team pays, the PI should lock legal entity, beneficiary name, bank annex, spec annex, artwork approval, lead-time start, deposit trigger, balance trigger, and bank-change rule.

A normal deposit-plus-balance structure is not the problem. The problem is paying before the order file is complete. For custom golf ball payment terms, the PI should do more than list price and quantity. It should connect money release to the exact product your team approved.

The spec annex should cover construction, material family, weight, diameter, compression or hardness where applicable, coating, logo, packaging, carton marks, and compliance requirements. The artwork annex should include source file, Pantone or color target, logo position, logo size, color count, packaging file version, and sample proof. For custom logo golf balls payment, this is not design housekeeping. It is payment evidence.

Lead time should also be written clearly. Many factories count lead time from deposit received plus spec and artwork approval, not from the PO date. Put that start condition in the PI so nobody argues later when an event date, pro-shop launch, or corporate gift deadline is coming fast.

Ask the supplier to attach a signed PI/payment-control annex that states legal entity, beneficiary name, fixed bank details, spec annex, artwork approval, lead-time start condition, deposit trigger, PSI-based balance trigger, shipping-document trigger, and bank-change amendment rule.

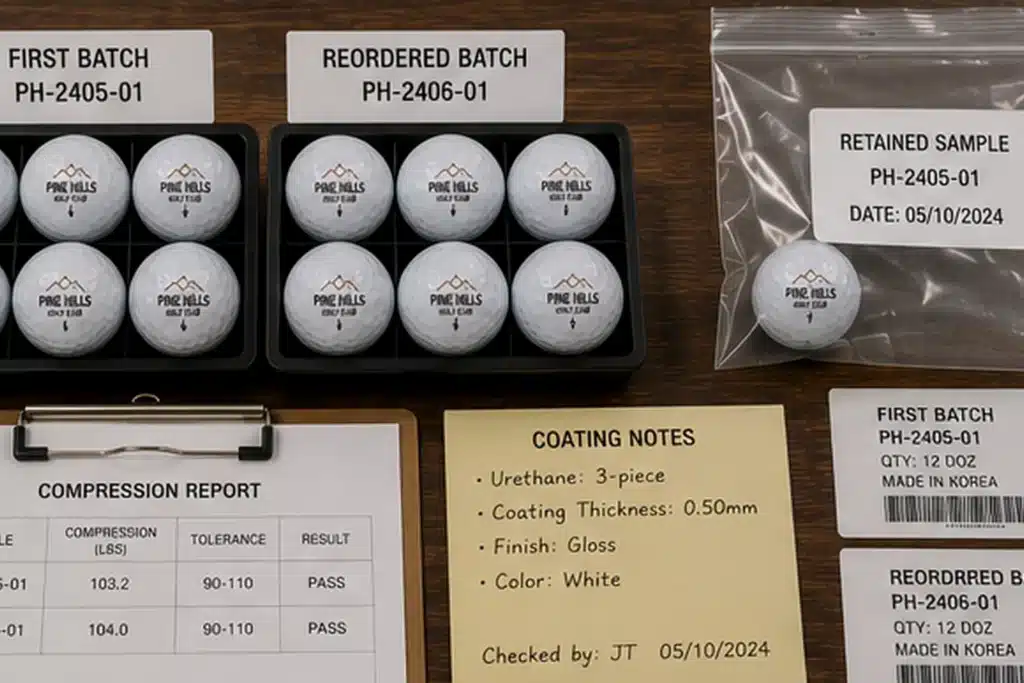

Supplier shall link legal entity, beneficiary name, signed PI, fixed bank details, bank-annex version, spec annex, artwork version, approved sample, retained sample, PSI report, batch ID, carton labels, and shipping documents under one auditable order record.

Deposit is requested before spec, artwork, and bank annex are locked is a failure signal.

| Pain/decision | PI lock item | Why it matters | Action/evidence |

|---|---|---|---|

| Deposit pressure | Signed PI | Defines order scope | Save signed copy |

| Bank confusion | Bank annex | Locks beneficiary | Match vendor file |

| Spec drift | Spec annex | Defines pass/fail | Attach version |

| Logo dispute | Artwork annex | Locks file/color/size | Approve sample |

| Lead-time argument | Start condition | Prevents PO-date dispute | Write trigger |

| Future bank change | Amendment rule | Stops email edits | Require signed update |

✔ True — 30/70 terms need triggers

A deposit percentage is only useful when the PI states what must be approved before deposit and what proof releases the balance.

✘ False — “The deposit percentage defines payment safety”

A 30% deposit can still be unsafe if bank details, artwork, specs, lead-time start, and sample approval are not locked in writing.

Lead time, spec annex, and bank annex?

Your deposit should buy a locked plan, not an argument about what everyone thought was approved.

Ask for the signed PI, bank annex, spec annex, artwork proof, lead-time start condition, and payment-trigger clause before deposit. Then check whether the legal entity, beneficiary name, bank account, PI, and vendor file match exactly.

Do not pay the deposit until bank details, specs, artwork, and lead-time trigger are version-controlled in writing.

When should you release the balance?

You may receive photos and a packing list and feel pressure to release the balance, but first-order balance payment is your last meaningful control before goods leave factory control.

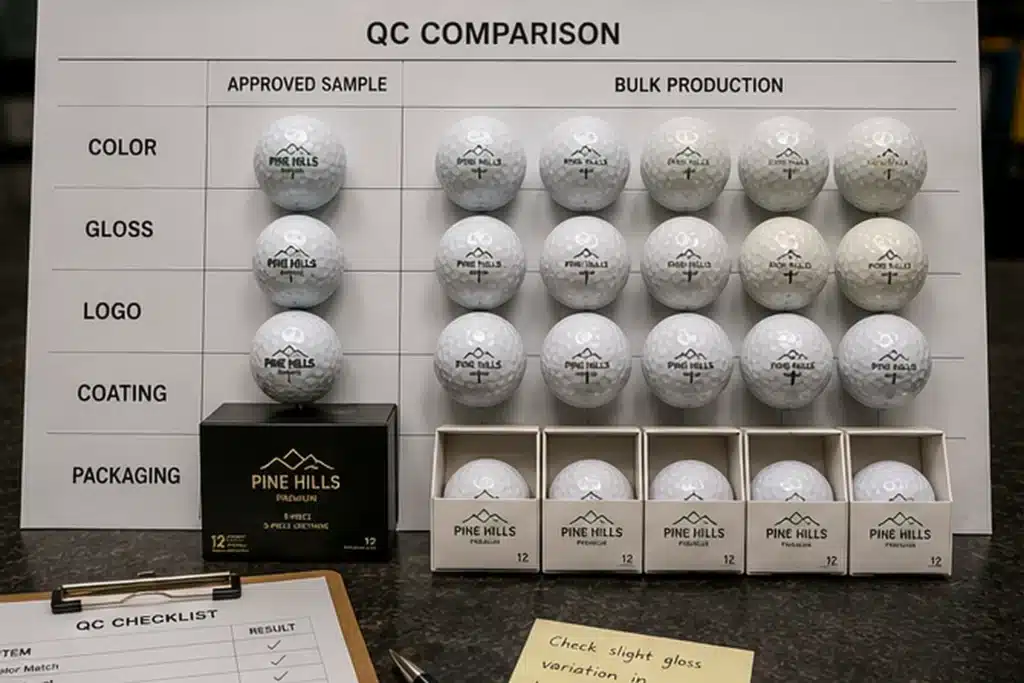

Release the balance after proof, not after photos. For a first golf ball OEM order, your team should use PSI pass, approved-sample comparison, logo/packaging checks, retained sample, and verifiable shipping documents before the final wire leaves your control.

Photos can support payment review, but they should not replace inspection on a first order. A packing list can show what the supplier says was packed. It does not prove logo color, position, carton marks, packaging quality, visible defects, or basic golf ball checks against the approved sample.

Your PI should state the balance trigger clearly: balance after PSI pass plus verifiable shipping documents. For golf ball pre-shipment inspection, the check should include quantity, carton count, visible defects, logo position, logo color, logo size, packaging, barcode or carton marks, and match against the approved sample. Where practical, include agreed golf ball checks such as weight, diameter, compression or hardness, and simple surface or logo durability checks.

Logo durability deserves special attention. UV printing, pad printing, coating, ink, curing, and surface treatment all affect adhesion. Print method is not proof; test result is proof. If the product is for a corporate event, academy program, or pro shop shelf, add logo rub or abrasion checks before balance release.

AQL-based inspection can help turn “looks good” into sample-based pass/fail language. ISO 2859-1:2026 provides AQL-indexed sampling schemes for inspection by attributes, so it can support sample-based PSI language without turning this article into a full QC guide.

Supplier asks for balance after photos but before PSI is a failure signal.

| Pain/decision | Release proof | Why it matters | Action/evidence |

|---|---|---|---|

| Photos only | PSI report | Objective pass/fail | Hold balance |

| Short shipment risk | Quantity/carton count | Protects PO value | Check counts |

| Logo mismatch | Logo/color/position check | Protects brand | Compare sample |

| Weak print | Rub/abrasion check | Avoids logo claims | Record result |

| Wrong pack-out | Packaging/carton marks | Protects event/retail | Verify photos |

| Shipping dispute | Draft B/L/forwarder proof | Confirms movement | Match entity |

PSI, shipping docs, and retained samples?

Your balance payment is not a reward for progress. It is your last gate before shipment.

Request the PSI report, approved-sample comparison, logo proof, packaging photos, carton marks, retained sample, and shipping-document proof before balance. Then check whether PSI results match the exact spec annex and artwork version attached to the PI.

Balance payment shall be released only after PSI pass and verifiable shipping documents, with inspection covering agreed quantity, carton marks, packaging, logo position/color/size, visible defects, and agreed golf-ball checks against the approved sample and spec annex.

After the wire, ask your bank for the UETR or MT103 where supported. A UETR is a 36-character reference used in Swift payment messages and can help banks trace international payments, but it tracks a payment after sending; it does not prevent fraud before sending. Unique End-to-end Transaction Reference

Do not release balance if PSI fails, the sample changes, or shipping documents do not match the contract party.

What red flags should stop payment?

You may face urgent requests, new bank details, beneficiary mismatches, personal accounts, or vague explanations right before payment, and your team needs a simple stop rule.

A new bank account by email is a hard stop, not an update request. Your AP team should pause payment for beneficiary mismatch, personal or third-party accounts, urgent pressure, refusal of PSI, or any bank change without known-contact verification and signed amendment.

Bank-detail change is where many normal-looking transactions become dangerous. Public guidance on business email compromise warns buyers to verify payment and purchase requests in person or by phone where possible, and to verify changes in account number or payment procedure with the person making the request.

That means no bank change may be approved by email alone. Your rule should require known-contact phone or video verification, signed bank-annex amendment, second AP approver, and saved call log. Use a phone number or contact path your team already has, not a new number provided inside the change-request email.

Beneficiary mismatch also stops payment. The legal entity, contract or PI name, beneficiary name, and AP vendor file should match. If the supplier asks you to pay a personal account, unrelated company, or third party, treat it as do-not-pay unless formal authorization, signed amendment, and internal exception approval exist. Even then, risk rises.

Urgency is a fraud pattern, not a reason to bypass controls. Small-business scam guidance warns that fake invoices and pressure to pay can make routine-looking bills dangerous. Scams and Your Small Business

New bank account is requested by email only is a failure signal.

| Risk event | Buyer response | Payment status | Action/evidence |

|---|---|---|---|

| Beneficiary mismatch | Reconcile legal entity | Hold | Match PI/bank |

| New bank by email | Phone/video + amendment | Hard stop | Save call log |

| Personal account | Reject or escalate | Do not pay | Require authorization |

| Photos only | Request PSI | Hold balance | Wait for pass |

| PSI failed | Rework/reinspect | Do not release | Agree remedy |

| Urgent pressure | Escalate AP/sourcing | Hold | Document exception |

✔ True — Bank-change control protects legitimate payments

A real supplier can still be affected by email compromise or invoice manipulation. Independent verification protects both sides before money moves.

✘ False — “A familiar email thread is enough proof”

Email threads can be spoofed, forwarded, or compromised. Bank changes require out-of-band confirmation and a signed amendment.

Bank changes and beneficiary mismatches?

Your finance team should treat uncertainty as a stop signal, not a customer-service problem.

Create an AP do-not-pay checklist for bank change, beneficiary mismatch, personal accounts, urgency pressure, no PSI, and inconsistent documents. Then verify bank-change requests through a known phone or video channel and save the call log plus signed amendment.

No bank detail may be changed by email alone; every change requires independent verification and second approval.

How do you scale after the first order?

You may want easier repeat payments after a successful first order, but terms should simplify only after batch history, inspection results, and supplier behavior prove stable.

Make the first payment system stricter than the repeat-order system. Once batch records, retained samples, PSI history, logo performance, communication behavior, and delivery reliability are stable, your team can simplify admin, but proof should not disappear.

The first order is not just production; it is a test of product, payment, communication, and documentation. Your first payment controls should be strict because the supplier has not yet proven sample-to-bulk consistency, logo durability, packaging accuracy, and on-time behavior.

Build a repeat-order file. It should include supplier name, legal entity, beneficiary record, production date, batch ID, retained sample, PSI result, logo proof, complaint history, delivery status, and payment record. This file lets your team compare future batches against approved samples instead of starting from memory.

Repeat trust should reduce admin, not remove proof. A reliable supplier may earn faster internal approval, but bank-change control should never disappear. A cheaper repeat quote should also be reviewed carefully. Low price is not payment safety if it removes QC, coating control, material consistency, or production priority.

If a supplier says funds were not received, trace before resending. Use bank receipt, beneficiary name, value date, UETR or MT103 where supported, and supplier receipt confirmation. Do not send a second payment because someone says the first one is “missing.”

| Pain/decision | First order control | Repeat-order adjustment | Action/evidence |

|---|---|---|---|

| No history | Full PSI | History-based scope | Keep proof |

| Sample drift | Retained sample | Compare batch | Link to PO |

| Logo risk | Rub/adhesion check | Spot check | Record result |

| Wire dispute | Bank receipt/UETR | Reuse vendor file | Trace, do not resend |

| Low-price pressure | Full evidence gates | Negotiate scope | Avoid blind cuts |

| Supplier stability | Strict milestones | Faster approval | Track performance |

Trial order, batch record, repeat payment?

Your repeat-order trust should be earned by evidence, not by comfort.

Maintain a repeat-order file with batch ID, retained sample, PSI result, logo proof, complaint history, delivery status, and payment record. Compare repeat production against the approved sample and prior batch data before relaxing any payment gate.

Do not simplify payment terms until inspection history and supplier behavior support it in writing.

FAQ

Is T/T safe for a Chinese golf ball order?

Yes, T/T can be safe when it is controlled. The risk is not the wire itself; the risk is wiring to the wrong beneficiary or releasing funds before evidence exists.

Match the legal entity, PI, and beneficiary name before payment. Lock bank details in a signed annex and AP vendor file. Release the balance only after PSI pass and verifiable shipping documents. Uncontrolled T/T is risky; verified-company T/T with release gates is a normal B2B settlement tool.

What is the safest payment method?

No method is automatically safest. T/T, escrow, L/C, and card payments all need identity checks, locked bank details, milestone triggers, and proof before release.

Use low-exposure methods for samples. Use verified-company T/T or escrow for many first bulk orders when evidence gates are written clearly. Consider L/C when order value makes document control worth the cost and time. The safest method is the one your team can actually control.

What deposit terms are normal for custom balls?

Deposit-plus-balance terms are common, but the percentage is less important than the trigger. Your deposit should follow a signed PI, spec annex, artwork approval, and fixed bank details.

Define when lead time starts. Attach spec and artwork versions. Reset the milestone if the sample fails instead of accepting “bulk will be better” as a promise. A normal deposit can still be unsafe if it starts before the order file is locked.

What if the supplier changes bank details?

Stop immediately. Do not approve new bank details by email alone; verify through a known contact path and require a signed bank-annex amendment.

Use phone or video confirmation through an existing trusted contact, not a number inserted into the change email. Add a second AP approver. Save the call log and signed amendment with the PO. No urgency should override this rule.

Can I release balance after photos?

For a first order, photos and a packing list should be supporting evidence only. Use PSI pass and verifiable shipping documents as the balance-release gate.

Check quantity, logo position, color, size, packaging, carton marks, and approved-sample match. Where practical, include basic golf ball checks such as visible defects, weight, diameter, compression or hardness, and logo adhesion. Hold balance if PSI fails.

Do FOB, CIF, or DDP decide payment timing?

No. Incoterms define delivery responsibilities, costs, and risk allocation; they do not replace deposit, balance, or payment-release clauses.

Trade guidance describes Incoterms as rules that clarify tasks, costs, and risks for buyers and sellers, including shipment, insurance, documentation, customs clearance, and logistics responsibilities. Payment triggers must still be written separately in the PI or contract.

What should be in a golf ball PI annex?

A useful PI annex should lock legal entity, beneficiary name, bank details, construction, material, weight, diameter, compression or hardness where applicable, coating, logo, packaging, artwork, lead-time start, and payment triggers.

Attach versioned artwork. Define inspection requirements. Include the bank-change amendment rule. For custom logo golf balls, include logo source file, Pantone or color target, position, size, color count, packaging file, sample proof, and any logo durability check.

Can repeat orders use simpler payment terms?

Yes, but only after stable batch records, retained samples, inspection history, communication behavior, and delivery performance exist. Repeat trust should reduce admin, not remove proof.

Keep batch ID and retained sample records. Track complaints, PSI results, logo performance, and delivery reliability. Never remove bank-change controls. A repeat order should feel smoother because evidence exists, not because the team stopped checking.

Conclusion

Safe payment is not a payment method. It is a control system: verify the beneficiary, lock bank details, attach specs and artwork to the PI, release money only on proof, require PSI before the balance, and stop every bank-change request until independently verified.

For Chinese golf ball OEM sourcing, the safest buyer is not the most suspicious buyer. It is the buyer whose AP, sourcing, QC, and logistics teams know exactly what proof must exist before each payment milestone moves.

Start strict on the first order, keep clean batch records, and let repeat-order trust grow from evidence. That protects your money, your launch calendar, your logo quality, and the supplier relationship you actually want to build.

You might also like — How to Choose a Reliable Golf Ball Manufacturer in China?